We explored the two appraisal reports attached to the Capital City Country Club golf course, and we discovered some inconsistencies which may not change the value of the land, but do call into question the City of Tallahassee’s (City) review of these reports as well as the information the Country Club provided the appraisers. The City does have a licensed appraiser on staff to review these reports and ensure the reports are accurate and in the best interest of our community. In fact, We have an entire real estate department employed to protect our public assets. The Country Club has asked the City if they can purchase the golf course as they already own the clubhouse and the land on which it sits.

Before we begin, we must understand what an appraisal report is. According to a quick Google search1 we see that it is a written document by a licensed professional that estimates a property value based on its features, location, and comparable sales. We can think of this as a supported professional opinion. We emphasize that the support for the opinion. If the owner does not provide the information to the appraiser, they cannot provide an accurate valuation of the appraisal.

Appraisal Report I Prepared by Bell, Griffith & Associates, Inc. For Capital City Country Club2

We want to preface this section with a few important details to keep in mind. 1) The City Commission met after the completion of this appraisal. During their meeting, they directed staff to implement a deed restriction that keeps the property a golf course 2) The appraiser was very clear that the stated intention of this appraisal was for internal financial use. This means that the City cannot use it as a second appraisal and when the Country Club submitted it to the City for consideration, they violated the stated use of this report.

On September 8, 2025, the appraiser completed this report. This was about ten days prior to the September 17, 2025 City Commission meeting, when we learned of the possible sale of the golf course. The first appraisal states that the lead appraiser previously appraised the Country Club. We do see the designation MAI after his name. The appraisal institute gives this designation and implies rigorous standards for education and experience. This report does not note any other experience appraising golf courses or land of similar zoned use or size which is not required, but is standard.

An appraisal report is a supported opinion of value. Including qualifications adds support to the opinion.

This first appraisal states the property is “fee simple.” The term fee simple is the highest and most complete form of property ownership. This grants the owner indefinite and unrestricted rights to use, possess, sell and pass property to heirs. This type of ownership may still be subject to deed restrictions and easements. However, this appraisal doesn’t mention any restrictions. We do have to keep in mind that this appraisal was completed prior to the City Commission meeting and appears to be written for internal use. This form of appraisal is considered appraised as “value in use” as opposed to “market value” (which is highest and best use).

Close to a decade ago the identification and location of a historic cemetery became known to the City and the Country Club. Neighbors are still fighting for a memorial and respect for the site, recently spilling into the news again. Some questions we have here: Why didn’t the Country Club disclose this to the appraiser? What should also be addressed is why did the appraiser not know this information as it is of particular interest to the public and has been for some time?

Reading through intended use of the appraisal (page 12), this report explicitly states that “no purchasers, sellers, or borrowers of the subject property are intended users of this appraisal.” It also explicitly states that this appraisal is strictly prohibited for use other than the intended user. This means that the City is prohibited from using this appraisal for sale of the property, and this shouldn’t be considered a second appraisal by the City.

On page 44, this report mentions the highest and best use for the property being residential development (remember, this appraisal was done prior to the discussion of a deed restriction and “is for internal review and/or financial decisions” page 12). However, the report does not provide any residential development sales compared to golf course sales. Providing that information would make the argument of higher and best use being residential development more compelling. This inconsistency conjures up questions regarding what the number in this report is trying to reach? The best use of the land or the use of the land being a golf course?

The report references four golf course sales. Three are in Florida and one is in Georgia. However, Killearn Country Club golf course, which sold in 2022, is not mentioned or discussed as to why it wasn’t considered. The reason may have been acceptable but without an explanation we don’t know the reason the appraiser omitted it. We can assume it is due to the building and amenities sold with the golf course and because the Country Club does not have a club house located on it. This particular property does not include the current clubhouse as that is owned by the County Club. However, the comparable sales used do contain club houses, bars, restaurants, pools, tennis courts, and shops (pg46-53).

Finally on the first appraisal we see projected revenues stated as the course “past operating historical rounds” at 20,000 rounds. But then the author calculates the revenue by $25.00 (green fee rate) by the rounds they use 25,000 rounds. This could simply be a simple typing error (we have had our fair share in our work). Yet, it still adds to the inconsistencies in the report.

Appraisal Report II Prepared by CBRE Valuation and Advisory Services For The City3

The second report is done by an appraisal firm in Jacksonville. It appears that it was written by a senior appraiser (located in Tallahassee) and a vice president reviewed it. The senior appraiser does not have MAI but the vice president does. This report does have substantially more comments about golf course appraisals, which gives the impression they have adequate experience appraising golf courses.

It is also important to note that the appraiser states he is basing his valuation on the assumption the subject property would be deed restricted to golf course use and that no redevelopment to a different use would be allowed. One important note is that this report was completed October 8, 2025, after the September 17 meeting. We can assume that the city told this Appraiser of the deed restriction that the City Commission would implement.

This appraiser also worked under the assumption that the lease would be voided upon sale of the golf course and the buyer (Country Club) would acquire fee simple title with a deed restriction.

However, there is also no mention of the historic cemetery in this report. Again, given the public interest in the historic cemetery and the media coverage around it, this should have been common knowledge and therefore identified in the report with the size and legal restrictions that might be imposed on that part of the land. On pages 13 and 14 there is a site summary but even here the historic cemetery is not discussed or acknowledged.

This report differs from the numbers in the first report on the number of rounds. This report shows twice as many rounds. This particularly calls into question the Country Club and what they are reporting to both appraisers. We were unable to locate how this author came to conclude 40,000 stabilized rounds but he did state that detailed income and expense figures were not provided to him from the Country Club. Nevertheless, on page 53 the appraiser reports he based his estimate of a gross income multiplier on the subject’s historical operations and limited revenue. We must ask why they were not provided? A small increase in number of rounds could significantly increase the value, making it more desirable. Without support for the estimated number of rounds it is difficult to follow the appraiser’s logic.

On page 4 we see that round data was reportedly from a “prior appraisal (third party), but considering the impact on value of the estimated rounds the appraiser should include an analysis of that data and confirm why they find it reliable enough to use in their report.

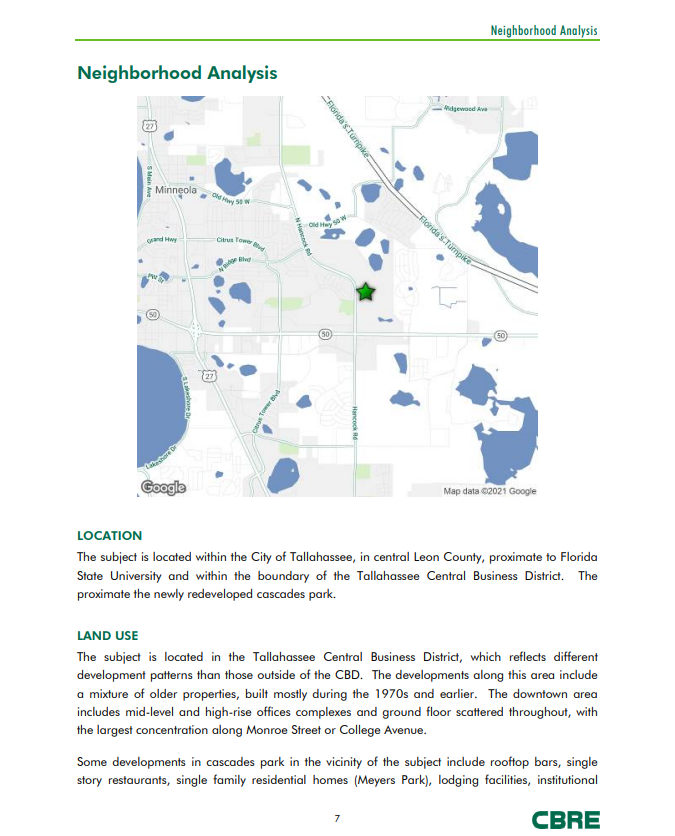

On page 7, the neighborhood map used in the report isn’t for Leon County and shows the Florida Turnpike in Minneola FL about 237 miles south of Tallahassee. While this could be a simple error it certainly instills doubt in the rest of the report’s accuracy. It also makes us question the City’s review process of these reports and their thoroughness.

This appraiser reports competitive green fees and lists a table on page 42. The weekday green fees are $75 but there isn’t any amount listed for the weekend. We also noticed that the appraiser uses the Country Club as one of the comparatives and then under the “subject” he concludes $40-50 for the Country Club on weekdays and $50-60 on weekends. He goes on to explain that the subject is inferior to Southwood ($40-50 weekday and $55-70 on weekends) and superior to Hilaman ($30 weekdays and $45 weekends). However, the next page reports Hilaman generating more rounds per year in FY24 and FY25. This calls into question the number of rounds that the appraiser concluded.

Comparable sales in this report on page 50 do not have a detailed sale sheet included for the 15 comparable sales listed. They did not include whether the sales were fee simple estates or had the potential to be developed into anything other than a golf course later. The sales here ranged from February 2021 to December 2024. And these sales were from all over the country. Again, Killearn was not included in this report and there was no explanation as to why. Without an explanation as to why it wasn’t included, we are unable to understand the appraiser’s thought process.

The City’s Responsibility

The City has a responsibility to review these reports for consistency and accuracy prior to accepting them as completed. There is obvious pertinent information missing from these reports that shapes the estimate. Furthermore, the City cannot use the first report as it explicitly states that it is not intended for the seller’s use. We also need to ensure that all information is provided to the appraisers in full. These reports are missing the historic cemetery as well as relevant information on the number of rounds.

The appraiser can only have an accurate supported opinion if all of the information they require is produced. Without the information needed, their report is inconsistent and misses substantial information. We are also concerned about other appraisals that the City has acquired. Particularly the sale of our community hospital TMH. If the City excludes information or does not review the appraisals thoroughly on our golf course, how much more are they missing on our hospital?

We are better together, keep the conversation going.

- Consumer Financial Protection Bureau, “What are appraisals, and why do I need to look at them?,” September 4, 2025, ↩︎

- Bell, Griffith & Associates, Inc appraisal for Capital City Country Club, September 2, 2025, Stephan A. Griffith, MAI ↩︎

- CBRE Valuation & Advisory Services appraisal for City of Tallahassee, October 8, 2025, Michael (Mace) J. Green, Jr and Brent Scott, MAI ↩︎